Langley Accounting FAQ

Questions from Langley Business Owners and Farmers

Simple answers to the questions we hear most often from Langley's farms, trades businesses, and families.

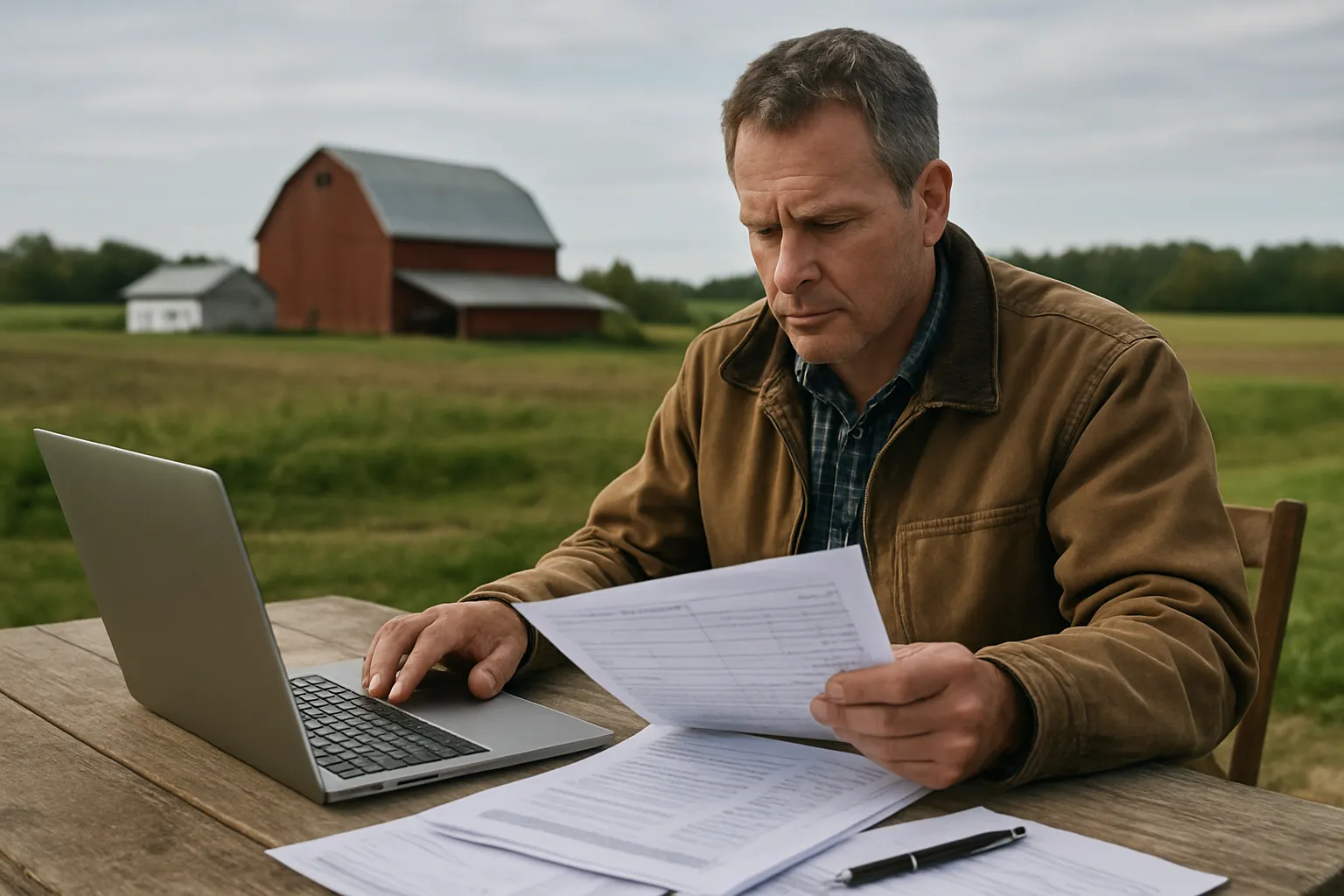

How is farm income taxed differently from regular business income?

Farm income is reported on the T2042 Statement of Farming Activities, which is added to your T1 personal return. One key difference is the option to use cash basis accounting. This means you report income when cash is received and deductions when cash is paid, rather than when transactions are earned or owed. That can be useful when you want to shift income between tax years. There are also specific rules for AgriStability and AgriInvest, which are federal programs that help stabilise farm income. Both require accurate financial records to participate. Phoenix Knight sets up farm bookkeeping that meets those requirements from the start.

I run an equestrian or horse property in Langley. Does that count as a farm?

It can — but the rules are specific. CRA considers an operation a farm if it is carried on with a reasonable expectation of profit and is an ongoing business activity. Simply boarding horses or living on a rural property does not qualify. However, breeding, training, or selling horses as a business generally does. If you have an equestrian operation in Langley Township, we review the activity, help you document it correctly, and make sure the expenses are claimed in a way that CRA is likely to accept. We have worked with equestrian and agri-business operators in the Langley area before, so we understand what the records need to look like.

What is AgriStability and do I need to apply every year?

AgriStability is a federal program that pays out when your farm income drops by more than 30% compared to your average income in recent years. It is designed to help during a bad crop, market downturn, or unexpected loss. To participate, you must enrol by a specific deadline each year and file the required program documentation. The key to a successful claim is having accurate, well-organised financial records that match your T2042 farm income return. Phoenix Knight prepares the financial records Langley farmers need to participate in AgriStability and helps with the application documentation where needed.

When should I consider incorporating my Langley trades business?

The short answer is when your business earns more than you need to live on each year. Money left inside a corporation is taxed at 11%, not at personal rates that can be much higher. If you are making $100,000 in profit but only need $70,000 to cover your living costs, the remaining $30,000 could be retained in a corporation at a much lower tax rate. We model the actual numbers for your income level before recommending anything. There are also non-tax reasons to incorporate — like separating your personal assets from business debt — that matter for trades businesses in Langley where job risk is real.

We are planning to transfer our Langley farm to our children. What do we need to do?

Start planning at least two to three years before the intended transfer date. There are specific rules around how long farm property must have been used in a farming business, how the transfer is structured, and whether a share sale or an asset transfer is better for your situation. The Lifetime Capital Gains Exemption can protect up to $1.25 million of the gain from tax — but only if the property qualifies and the conditions are met. We also look at whether holding the farm in a corporation versus personally affects the available exemption. The rules changed significantly with Bill C-208, and planning ahead gives you options that a last-minute transfer does not.